When people apply for or use credit cards in the United States, they often focus on rewards programs, interest rates, and sign-up bonuses. However, many cardholders overlook the less visible charges that can quietly accumulate.

These hidden fees can eat away at your budget if you are not careful, making it essential to understand how they work and what to do about them. With the right tips, it becomes much easier to protect yourself from unpleasant surprises.

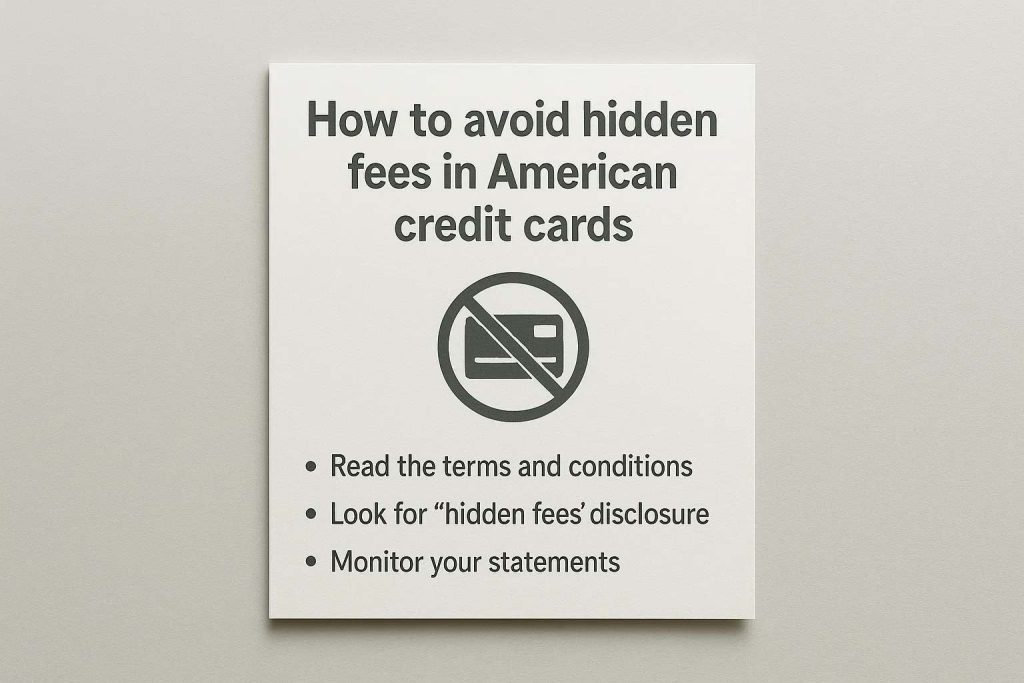

Understanding common hidden charges

Many credit cards carry fees that are not always obvious to new users. Annual fees, late payment penalties, and balance transfer charges are usually disclosed, but other costs such as foreign transaction fees, over-the-limit penalties, and expedited payment charges often come as an unpleasant surprise.

Another area where hidden fees appear is in convenience transactions. For example, using a credit card for a cash advance often comes with both a transaction fee and a higher interest rate that begins accruing immediately. Even services like expedited card replacement can include unexpected costs.

Reading the fine print carefully

Credit card issuers are required by law to disclose fees, but the details are often buried in the terms and conditions. Reading the fine print may feel tedious, but it is one of the most effective ways to prevent surprises. Look closely at sections dealing with penalties, balance transfers, and foreign transactions.

It is also wise to review monthly statements for any unfamiliar charges. Sometimes fees are applied under vague labels that make them hard to identify. If you see a charge you do not understand, contact your issuer immediately. By being proactive and questioning every suspicious item, you create a habit of monitoring your account and avoiding recurring unnecessary charges.

Choosing the right card for your needs

One of the best ways to avoid hidden fees is to choose a credit card that fits your spending habits. Some cards are designed for travelers, others for everyday purchases, and others for balance transfers. A mismatch between your habits and the card’s fee structure can lead to costly surprises.

Comparing cards also means looking beyond flashy perks. Many cards advertise generous cashback or travel rewards but quietly attach high annual fees or strict redemption rules. Before committing, calculate whether the rewards outweigh the costs in your particular case. Sites like NerdWallet provide comparisons that make it easier to see the real value of a card beyond its marketing claims.

Negotiating and monitoring fees

If you discover fees on your account, do not assume they are non-negotiable. Many issuers are willing to waive or reduce charges if you contact them directly, especially if you have a strong payment history. For example, a late fee may be forgiven if it is your first mistake, or an annual fee may be reduced if you express interest in closing the account.

Monitoring your account is equally important. Many banks provide mobile apps that send alerts for charges, due dates, or unusual activity. Setting up these notifications allows you to respond quickly and prevent small issues from snowballing. By actively tracking your spending and charges, you reduce the chances of hidden fees catching you off guard.

Building long-term financial habits

Avoiding hidden fees is not just about carefully selecting a credit card; it also involves developing strong financial habits. Paying balances on time, avoiding cash advances, and planning purchases with awareness of your card’s fee structure all contribute to reducing costs. Over time, these habits ensure that you are using credit as a tool rather than allowing it to become a burden.

Long-term awareness also means revisiting your card agreements periodically. Banks often update terms, and changes might introduce new fees or alter existing ones. Staying informed about these updates ensures that your strategy for avoiding hidden charges remains effective.