Economic cycles are inevitable, and concerns about a potential recession in the US have become part of financial discussions in recent years. While downturns bring uncertainty, they also present opportunities for those who prepare ahead of time. Building a strategy before difficulties arise allows individuals and families to face challenges with greater stability and less stress.

The best preparation involves balancing caution with discipline. Instead of reacting to sudden market declines, a proactive plan protects income, reduces exposure to debt, and strengthens long-term resilience. By anticipating the effects of a recession in the US, households can safeguard financial health and position themselves to recover faster when conditions improve.

Why preparing ahead matters

Economic slowdowns affect nearly every aspect of daily life. Job security may weaken, investment returns can shrink, and access to credit becomes more restrictive. For these reasons, having a plan is not optional; it is a necessity. Creating financial buffers ahead of time ensures that a family can maintain essential expenses, even if income drops temporarily during a recession in the US.

Another important reason to prepare is psychological. Financial stress intensifies in uncertain times, and the lack of planning often leads to rash decisions. By organizing resources in advance, individuals gain confidence to navigate volatility. Knowing that bills, savings, and essential needs are covered reduces anxiety and prevents costly mistakes during a downturn.

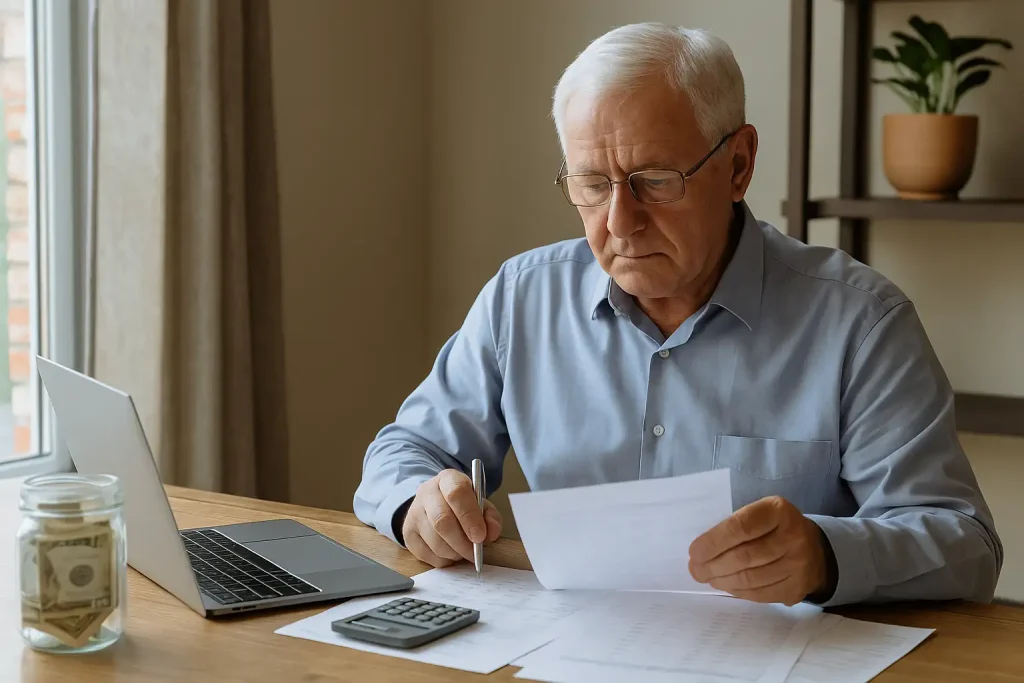

Key steps to strengthen your finances

Preparation does not require radical or overwhelming changes, but it does demand focus and discipline. Consistent small actions build resilience over time, creating a safety net when unexpected challenges appear. By developing healthy habits before a downturn strikes, households can rely on stronger foundations and reduce vulnerability during a possible recession in the US.

- Build an emergency fund covering at least three to six months of expenses.

- Reduce high-interest debt to lower financial vulnerability.

- Diversify income streams to avoid relying on a single source.

- Review and adjust investments to balance risk and security.

These measures provide a cushion when the economy contracts significantly. Instead of scrambling to find solutions in the middle of a recession in the US, those who prepare early can adapt more calmly and protect their essential long-term financial goals.

Managing debt wisely

Debt becomes especially risky during downturns. Credit may tighten, interest rates may rise, and repayment capacity may decline. To avoid pressure, individuals should prioritize paying off expensive obligations like credit card balances. Refinancing or consolidating loans before conditions worsen can also provide relief. Taking a proactive approach to debt management ensures greater flexibility and stability during a recession in the US.

Investing with caution

Recessions often bring volatility to financial markets, but that does not mean investors should abandon their strategies entirely. The key is balancing growth with protection. Defensive sectors, such as utilities or healthcare, tend to be more stable, while maintaining some exposure to long-term investments allows portfolios to recover when the economy stabilizes.

Investors should also reassess their tolerance for risk. Aligning portfolios with realistic objectives prevents panic selling when markets fluctuate. Maintaining discipline during a recession in the US is essential to preserving capital and preparing for recovery.

Final considerations

The possibility of a recession in the US is a reminder that financial security depends on preparation rather than prediction. While no one can fully anticipate the depth or duration of an economic downturn, individuals can control how ready they are to face it. Building savings, reducing debt, and adjusting investments are all practical steps that strengthen resilience.

Ultimately, the best strategy is consistency. By adopting healthy financial habits today, households are better equipped to withstand challenges tomorrow. In this sense, preparation turns uncertainty into an opportunity to build discipline and long-term stability.