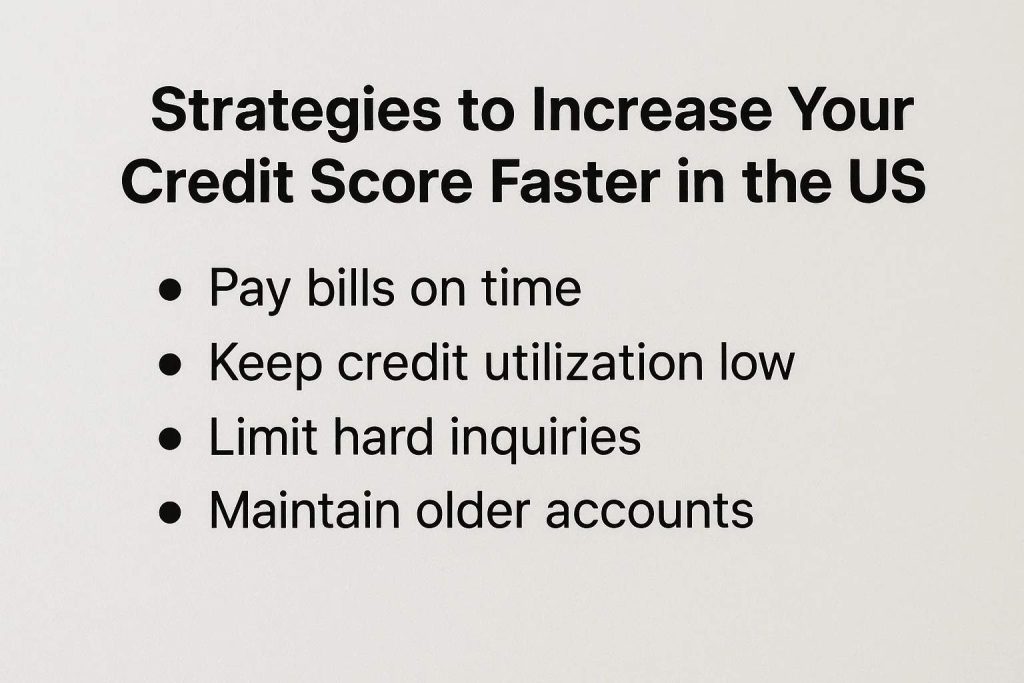

Improving your credit score in the United States can feel like a long and challenging process, but there are practical ways to accelerate your progress. With the right strategies, you can see noticeable results within months rather than years. Understanding the mechanics behind credit scoring and applying specific tips consistently will help you strengthen your financial profile and gain access to better credit opportunities.

A higher credit score not only boosts your chances of loan approvals but also helps you qualify for lower interest rates, better credit card offers, and even rental applications. For many people, the process of improving their score seems vague, but by applying focused methods, you can gain momentum more quickly. The following sections will guide you through proven approaches to raise your score efficiently while avoiding common pitfalls.

Focus on timely payments

One of the most influential factors in your credit score is your payment history. Even one late payment can significantly harm your score and remain on your credit report for years. To speed up your credit growth, it is essential to ensure that every bill—credit cards, personal loans, utilities, or mortgages—is paid on time.

Consistency is the key. Over time, lenders and credit bureaus begin to recognize a pattern of responsibility. If you currently have any overdue accounts, bringing them current as soon as possible can immediately reduce the negative impact on your score. From that point forward, a flawless payment history will start working in your favor.

Reduce credit utilization

Credit utilization refers to the percentage of your available credit that you are currently using. This factor accounts for a substantial portion of your credit score calculation. Keeping your utilization ratio below 30% is often recommended, but if you want to accelerate score improvement, aiming for below 10% can yield stronger results.

Another approach is to request credit limit increases from your card issuers. If approved, this expands your total available credit, reducing your utilization ratio even if your spending remains the same. However, it is crucial not to use the increased limit as an excuse to overspend. The primary goal is to demonstrate financial responsibility by managing credit wisely.

Diversify your credit mix

Having different types of credit accounts can also improve your score. Credit scoring models tend to reward individuals who can manage both revolving credit, such as credit cards, and installment loans, such as car loans or student loans. This shows that you can handle different forms of borrowing responsibly. For those who have only one type of credit, diversifying may provide an additional boost.

That said, opening new accounts should be done strategically. Applying for too much credit at once can trigger multiple hard inquiries, which may temporarily lower your score. In many cases, securing a small personal loan or even a credit-builder loan through institutions like Experian can help balance your credit mix while also building positive payment history.

Manage credit inquiries carefully

Every time you apply for credit, a hard inquiry is placed on your report. While one or two inquiries have a small impact, multiple inquiries in a short period can lower your score and make you appear riskier to lenders. To speed up score growth, you should avoid unnecessary applications and only seek new credit when it serves a clear purpose.

Address negative marks strategically

Negative items, such as collections, charge-offs, or bankruptcies, can weigh heavily on your credit score. While some of these take time to fade, there are proactive steps you can take to minimize their impact. For instance, negotiating with a collection agency to pay off a debt in exchange for having the account marked as “paid” can make a difference. Although not always guaranteed, some creditors are willing to update reporting if you demonstrate a genuine effort to resolve the debt.